Bihar Student Credit Card Scheme (BSCC) 2024: Complete Guide, Interest Rates & Online Application

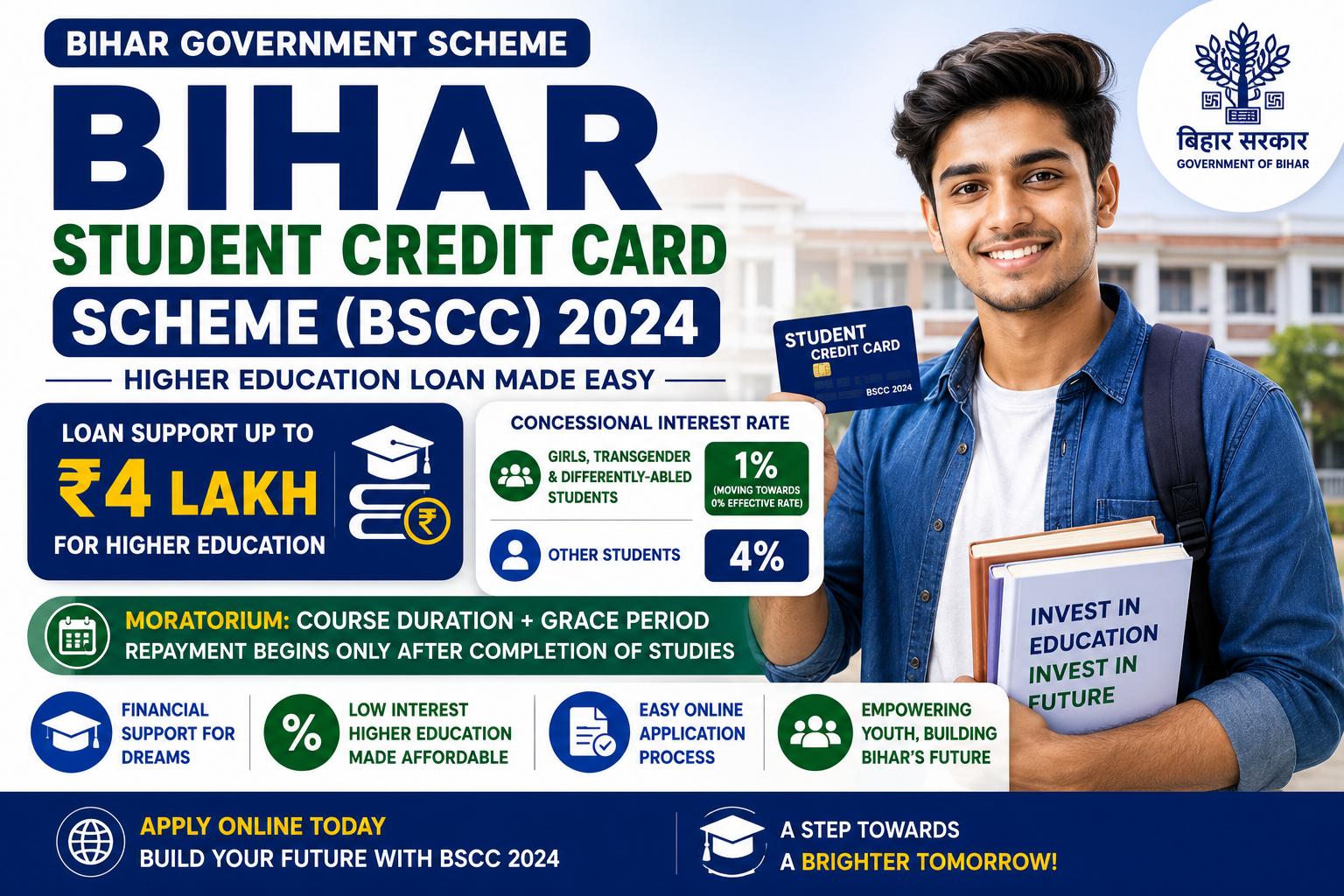

The Bihar Student Credit Card Scheme (BSCC) is a flagship higher‑education financing program launched under the Mukhyamantri Nischay Sapt Yojana (MNSSBY). Governed by the Education Department, Government of Bihar, this scheme offers up to ₹4 lakh in education loans to eligible students from the state at highly concessional interest rates.

The defining feature of this policy is its focus on social equity: girls, transgender individuals, and differently‑abled students enjoy a special 1% interest rate (with recent announcements moving towards a 0% effective rate). Furthermore, a generous moratorium period covers the entire course duration plus a grace period, ensuring that the financial burden of repayment only begins after the student’s education is complete.

Scheme Overview at a Glance

| Feature | Official Details |

|---|---|

| Implementing Authority | Education Department, Govt. of Bihar / MNSSBY |

| Scheme Name | Bihar Student Credit Card Scheme (BSCC) |

| Maximum Loan Amount | Up to ₹4,00,000 per eligible student |

| Legacy Interest Rates | 4% (General Male) / 1% (Girls, Transgender, Divyang) |

| Official Portal | 7nishchay-yuvaupmission.bihar.gov.in |

Key Benefits & Financial Assistance

The highly accessible loan limit and heavily subsidized interest structure form the core attraction of the Bihar Student Credit Card Scheme.

- Maximum Loan Amount: Students can avail of up to ₹4,00,000 to cover higher education costs in officially approved courses and institutions.

- Coverage of Expenses: The ₹4 lakh limit is comprehensive. It covers tuition fees, examination fees, and admission charges, alongside books, equipment, hostel charges, and other essential academic expenses.

- Legacy Interest Rate Structure: Historically, the scheme charges a 4% simple interest rate for general male students, while offering a 1% concessional simple interest rate for girls, transgender, and differently‑abled (Divyang) students.

- Recent Policy Shift (2025-2026): As per recent state announcements, Bihar has initiated a move towards 0% (interest‑free) education loans for all categories under the BSCC. However, many static scheme documents and bank guidelines still reference the legacy 4% vs. 1% structure.

Illustrative Benefit Snapshot

| Category | Loan Limit | Legacy Interest Rate |

|---|---|---|

| General (Male) | Up to ₹4,00,000 | 4% simple interest |

| Girls students | Up to ₹4,00,000 | 1% simple interest |

| Transgender students | Up to ₹4,00,000 | 1% simple interest |

| Differently‑abled (Divyang) | Up to ₹4,00,000 | 1% simple interest |

Who Can Apply? Eligibility Criteria

Eligibility for the BSCC is strictly defined around state domicile, age, education level, and the formal recognition of the chosen academic course.

- Domicile: The applicant must be a permanent resident of Bihar and possess valid domicile proof.

- Educational Qualification: The student must have successfully passed their 12th standard (Intermediate) from a recognized board.

- Institutional Approval: The applicant must have secured admission or selection in a recognized higher education institution (this includes state/central universities, recognized private institutions, and colleges approved by AICTE, BCI, MCI, or the University Grants Commission – UGC).

- Age Limit: Most official summaries indicate a maximum age limit of 25 years at the time of application. Certain relaxations may apply depending on the admission year, so the MNSSBY portal should be checked for the latest updates.

- Course Type: The scheme covers a vast range of general streams (BA, BSc, BCom) as well as professional and technical courses including Engineering, Medical, Law, Management, Polytechnic, and IT.

- Category Criteria for Concessional Rate: To avail of the 1% special interest rate, the applicant must legally fall into the female, transgender, or differently‑abled categories, supported by official certification.

- Non‑Duplication Condition: The student must not currently be availing of another major education loan, comprehensive scholarship, or overlapping student credit card covering the same course from other government sources.

Mandatory Document Checklist

To avoid processing delays or rejections at the verification stage, students must prepare a complete dossier of the following documents before starting their online application.

- Identity & Domicile: Aadhaar card of the student, a Bihar Domicile certificate, and an additional photo ID (e.g., voter ID, PAN card).

- Educational Documents: 10th and 12th standard mark sheets and passing certificates. An official admission/selection letter from the recognized college/university, along with a detailed fee structure/estimate issued by the institution.

- Category & Special Status Proof: A valid Caste certificate (SC/ST/OBC) if applicable. A disability certificate for differently‑abled students seeking the 1% rate, or corresponding documentation for transgender applicants.

- Income & Financial Documents: A family income certificate (current rules sometimes apply an upper-income threshold, often cited around ₹6 lakh per year). Guarantor or parent details as required by the partner financing agency.

- Banking & KYC: Active bank account details of the student and parent (passbook or cancelled cheque), alongside standard KYC documents as per the partner bank’s norms.

- Photographs & Signatures: Recent passport‑size photographs and clear scanned signatures of both the student and the parent/guardian.

Step‑by‑Step Application Process

The BSCC application is initiated online via the MNSSBY portal, followed by physical verification at a designated district center.

- Visit the MNSSBY Portal: Navigate to the official 7 Nischay / Bihar Student Credit Card portal (7nishchay-yuvaupmission.bihar.gov.in).

- Register as a New Applicant: Click on “New Registration.” Provide basic details such as your name, mobile number, email, and Aadhaar, and verify the session using an OTP.

- Fill the Application Form: Log into the dashboard and input your detailed personal, family, and educational information. Enter the specific course name, institution, and precise course duration. Specify your required loan amount (up to ₹4 lakh) and provide a detailed break‑up of the fees.

- Upload Documents: Upload high-quality scanned copies of all required educational certificates, admission proofs, domicile, caste/income documents, photographs, and bank details.

- Submit and Save Reference: Review all inputs meticulously. Submit the application and ensure you save or print the generated application reference number/acknowledgement for the counseling stage.

- Verification at the DRCC: Students will be summoned to their local District Registration and Counseling Centre (DRCC). You must bring all original documents for physical verification. Officials will confirm your eligibility and forward the approved file to the financing agency.

- Loan Sanction & Execution: The partner bank assesses the forwarded application. Upon approval, a formal sanction letter is issued specifying the exact loan amount and the applicable interest structure. The student (and guarantor/parent) signs the final loan agreements.

- Disbursement: The sanctioned loan amount is subsequently disbursed. This is often paid directly to the educational institution to cover tuition, with provisions made for hostel and book expenses within the approved limit.

Repayment & Moratorium Period

A major advantage of the BSCC is that students do not repay the loan during their active studies. The moratorium period covers the entire duration of the academic course plus a grace period of up to one year after course completion (or six months after securing employment, whichever is earlier). Once the moratorium expires, repayment begins in structured Equated Monthly Installments (EMIs), typically spread out over a generous period (e.g., 84 months / 7 years) to keep monthly payments highly manageable.

The Policy Intent

From a macroeconomic perspective, the Bihar Student Credit Card Scheme is a highly targeted intervention designed to break the systemic link between low family income and poor access to higher education. Historically, Bihar has witnessed severe dropout rates after class 12 due to financial constraints, resulting in a low Gross Enrollment Ratio (GER) in higher education and a persistent skills gap in the local workforce.

The BSCC rectifies this by guaranteeing up to ₹4 lakh in liquid education finance on incredibly soft terms. By offering a preferential 1% interest rate (transitioning toward 0%) for girls, transgender, and differently‑abled students, the scheme acts as a powerful social policy tool aimed at increasing gender equity and structural inclusion. The government anticipates that these cohorts will translate subsidized degrees into better employment outcomes, raising per‑capita household incomes and boosting female participation in skilled labor markets.

Frequently Asked Questions (FAQs)

Q1. What is the maximum loan amount under the Bihar Student Credit Card Scheme?

The maximum sanctioned amount under the BSCC is ₹4,00,000 per eligible student. This capital can be utilized for tuition fees, hostel accommodations, books, and other formally approved academic expenses at recognized institutions.

Q2. What is the interest rate for girls and transgender students under BSCC?

Under the legacy statutory structure, female, transgender, and differently‑abled students are charged a highly concessional 1% simple interest rate, compared to the standard 4% applied to general male students. However, recent policy announcements indicate a state push to make these loans completely interest‑free (0%) moving forward.

Q3. When does repayment start under the Bihar Student Credit Card Scheme?

Repayment does not begin immediately. Students benefit from a strict moratorium period that lasts for the full duration of their course, plus a grace period of either one year after graduation or six months after securing a job (whichever happens first). Following this, manageable EMIs begin over an extended period, usually 84 months.

Q4. Can I apply for the BSCC if I already have another education loan or scholarship?

Generally, the scheme strictly requires that students are not already utilizing another major education loan or an overlapping student credit card from other government sources for the exact same course. While students receiving minor merit or reserved-category scholarships may still apply, they must fully disclose all external financial aid during their DRCC counseling session.